Are you evaluating aluminum cookware for your import portfolio? The material science and market dynamics make this category increasingly attractive for savvy buyers.

Aluminum cookware represents a $11.8 billion global market with 6.8% CAGR through 2034, offering importers compelling cost advantages, diverse product applications, and strong consumer demand across both residential and commercial segments.

I've spent over 29 years in the kitchenware manufacturing industry, working directly with 500+ importers and distributors worldwide through INOXICON. Over this time, I've watched aluminum cookware evolve from a commodity product into a sophisticated category with significant profit potential. The key is understanding which aluminum grades, surface treatments, and market applications align with your target customers' needs and price points. Smart importers who positioned themselves early in premium aluminum segments have seen remarkable returns, while those focusing purely on low-cost options face increasing margin pressure.

What Aluminum Specifications Should You Prioritize for Maximum Market Appeal?

Do you know which aluminum alloys deliver the best balance of cost, performance, and customer satisfaction? The specifications you choose directly impact your competitive positioning.

3004 aluminum alloy with hard anodized finishing commands 40-60% higher wholesale margins than basic 1100 grade, while offering superior durability that reduces customer complaints and returns.

Working with manufacturers across different price tiers, I've learned that aluminum grade selection fundamentally determines your market positioning and profit potential. Basic 1100 grade aluminum works for entry-level products, but the market has largely commoditized this segment with razor-thin margins. The real opportunities lie in higher-performance alloys that justify premium pricing.

The 3003 alloy containing 1-1.5% manganese represents the sweet spot for mid-market positioning. This grade offers 30% better strength than pure aluminum while adding only 8-12% to raw material costs. Most importantly, it provides the durability customers expect from quality cookware, reducing warranty claims that can devastate profit margins. I've seen distributors achieve 35-40% gross margins on 3003 aluminum products compared to 18-22% on basic grades.

For premium positioning, 3004 alloy with manganese and magnesium delivers exceptional formability and strength. This specification works particularly well for European markets where consumers expect commercial-grade performance in residential cookware. The material cost premium runs 15-20% over 3003, but finished products can command 50-80% higher wholesale prices. The durability factor becomes crucial here - premium aluminum cookware should last 10+ years, and 3004 alloy consistently delivers this longevity.

Thickness specifications matter equally. I recommend minimum 2.5mm base thickness for serious cookware, with 3.0-3.5mm for premium lines. Thinner gauges reduce material costs but create customer dissatisfaction through warping and poor heat distribution. The cost difference between 2.0mm and 3.0mm base thickness is roughly 15%, but the performance and customer satisfaction improvements justify the investment.

Surface treatment selection determines your competitive differentiation. Hard anodized aluminum commands the highest margins - typically 60-80% above raw aluminum pricing - while providing genuine performance benefits. The process creates surfaces 30% harder than stainless steel, enabling metal utensil compatibility that customers value. Ceramic coatings offer PFAS-free positioning for health-conscious markets, particularly strong in European and North American premium segments.

How Do Coating Technologies Impact Your Profit Margins and Market Positioning?

Have you calculated the true cost versus benefit of different aluminum surface treatments? The numbers might surprise you.

Hard anodized aluminum cookware generates 65-85% higher gross margins than basic aluminum, while ceramic-coated products command 45-60% premiums, making surface treatment selection crucial for profitability.

Through my factory partnerships and client relationships, I've analyzed the economics of different aluminum coating systems extensively. The investment in surface treatments dramatically impacts both your landed costs and achievable selling prices, making this decision critical for portfolio success.

Hard anodization represents the premium positioning opportunity. The process adds approximately $3-5 per piece to manufacturing costs for typical pan sizes, but enables wholesale pricing 65-85% above basic aluminum. More importantly, anodized products generate fewer customer complaints and returns due to superior durability and stain resistance. I've worked with importers who built entire businesses around premium anodized aluminum, achieving consistent 45-50% gross margins across their product lines.

The key advantage lies in market differentiation. While basic aluminum cookware competes primarily on price, anodized products compete on performance and durability. This positioning protects you from low-cost competition while building customer loyalty and repeat purchases. European buyers particularly value anodized aluminum for its ability to withstand metal utensils and maintain appearance over years of use.

Ceramic coating technologies offer different strategic advantages. PFAS-free ceramic coatings address growing health concerns in developed markets, commanding 45-60% price premiums over traditional non-stick. The manufacturing cost increase runs $2-4 per piece, delivering strong margin improvements. However, ceramic coatings require more careful supplier selection as quality varies significantly between manufacturers.

Traditional PTFE non-stick remains the volume leader, but margin pressure continues increasing as the technology commoditizes. I recommend this option only for high-volume, price-sensitive segments where cost leadership is your primary strategy. The key is achieving sufficient scale to negotiate favorable coating costs while maintaining quality standards that minimize returns.

Emerging coating technologies present interesting opportunities for early movers. Sol-gel applications create incredibly durable surfaces that combine ceramic benefits with improved release properties. While still premium-priced, these technologies may become mainstream within 3-5 years, offering first-mover advantages for forward-thinking importers.

Where Are the Biggest Market Opportunities for Aluminum Cookware Imports?

Are you targeting the right geographic markets and customer segments? Market dynamics vary significantly across regions and applications.

Asia Pacific offers the largest volume opportunities at $4.6 billion market size, while North America provides the highest average selling prices and profit margins, particularly in the premium and commercial segments.

My experience working with importers across 50+ countries reveals distinct market characteristics that dramatically impact business success. Understanding these regional differences helps optimize your product mix, pricing strategy, and go-to-market approach for maximum profitability.

Asia Pacific dominates global volume with 38.6% market share, driven by massive population, growing middle class, and strong cultural preference for aluminum cookware in traditional cooking methods. However, this market remains highly price-sensitive with intense competition from local manufacturers. Success requires either extreme cost efficiency or specialized product positioning for premium segments. I've seen importers succeed by focusing on specific niches like induction-compatible aluminum or specialty shapes for ethnic restaurants.

North America presents the most attractive profit opportunity despite smaller volume. Average selling prices run 40-60% higher than Asian markets, with consumers willing to pay premiums for quality, durability, and brand positioning. The commercial segment offers particular promise - restaurant industry expansion and ghost kitchen proliferation drive steady demand for lightweight, efficient cookware. B2B sales typically generate 25-35% higher margins than retail due to volume purchasing and reduced marketing costs.

Europe combines reasonable volume with premium pricing, but regulatory complexity requires careful navigation. PFAS regulations continue tightening, creating opportunities for ceramic-coated and anodized products while challenging traditional non-stick options. German and Scandinavian markets show strong preference for durability and sustainability, supporting higher price points for quality aluminum cookware. The commercial segment remains robust, supported by strong restaurant culture and professional cooking education programs.

Emerging markets in Latin America and Africa present interesting long-term opportunities. While current purchasing power limits premium positioning, growing urban populations and improving economic conditions suggest future potential. Early market entry through cost-effective products can establish distribution relationships for eventual premium expansion.

Distribution channel evolution impacts market access significantly. E-commerce growth at 8.7% CAGR creates opportunities for direct-market entry without traditional retail relationships. Amazon alone captures 35% of US online cookware sales, offering importers direct access to consumers. However, success requires investment in digital marketing, customer service, and logistics capabilities that many traditional importers lack.

How Should Commercial vs Residential Applications Shape Your Product Strategy?

Are you optimizing your product mix for the highest-profit applications? Commercial and residential segments require different approaches but offer distinct advantages.

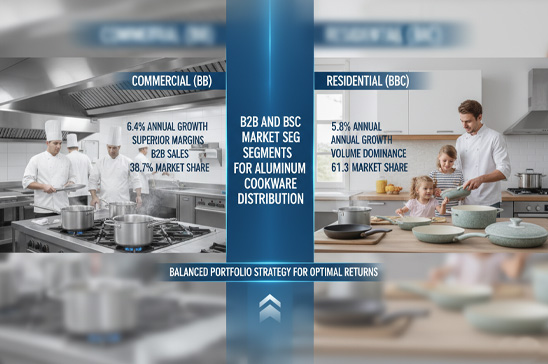

Commercial applications grow 6.4% annually versus 5.8% residential, offering superior margins through B2B sales while residential dominates volume at 61.3% market share, requiring balanced portfolio strategy for optimal returns.

Through my client relationships spanning wholesale distributors to foodservice suppliers, I've observed how successful importers balance commercial and residential opportunities. Each segment offers unique advantages, but the strategic approach differs significantly in terms of product specifications, pricing, and go-to-market execution.

The commercial segment provides superior margin stability and customer relationships. Professional kitchens prioritize performance and durability over aesthetics, enabling focus on functional excellence rather than expensive design features. B2B purchasing cycles are longer but more predictable, with established budgets and replacement schedules. Most importantly, commercial customers value supplier relationships, creating barriers to entry for competitors once you establish position.

Restaurant equipment dealers represent the primary distribution channel, typically working on 20-30% margins with established customer bases. Success requires building relationships with key dealers in target markets while providing technical support and competitive pricing. I've worked with importers who built substantial businesses by specializing in specific commercial applications - wok ranges for Asian restaurants, high-volume sauce pans for catering operations, or lightweight options for food truck applications.

Ghost kitchens represent an emerging commercial opportunity. These delivery-focused operations require efficient cookware that heats quickly and cleans easily in space-constrained kitchens. Aluminum's lightweight properties and heat responsiveness make it ideal for these applications. The ghost kitchen market numbers over 80,000 locations globally and continues expanding, particularly in urban areas with high delivery demand.

Residential applications dominate market volume but require different strategic approaches. Consumer purchasing behavior focuses heavily on aesthetics, brand positioning, and perceived value rather than pure functionality. This creates opportunities for premium positioning through design, packaging, and marketing investment. However, it also increases complexity through seasonal demand patterns, retail relationship requirements, and marketing costs.

The "prosumer" segment bridges commercial and residential applications, representing serious home cooks who seek professional-grade performance. These customers willingly pay commercial prices for superior cookware, creating high-margin opportunities without B2B complexity. Products targeting this segment should emphasize commercial heritage while providing residential-friendly features like attractive finishes and appropriate sizing.

Product format preferences vary significantly between segments. Commercial buyers focus on standardized sizes for kitchen efficiency, while residential consumers prefer variety packs and aesthetic coordination. Understanding these preferences helps optimize product development and inventory investment for maximum turnover and profitability.

Conclusion

Aluminum cookware offers compelling opportunities for importers through strong market growth, diverse applications, and significant margin potential when properly positioned across commercial and residential segments with appropriate quality specifications.